3 KICK-ASSet RRSP STRATEGIES

I’m going to show you how to get 20-66.66% more into your RRSP every year without saving any more money!

And to make this exciting (because writing financial strategies can be soul-wrenching-boring!), I have to relate my strategies to things that bring me joy.

Today, I was debating whether or not to compare these RRSP strategies to shoes or wine. Shoes won out, but just for today. So if you think like me, you will know flats are okay, kitten heels are a bit higher and mightier, but a night out on the town warrants killer sexy stilettos where your legs look fabulous and elongated (or that’s what I tell myself 😉 ) – even if you can only wear them for 5 minutes.

I also created a little chart at the bottom of this article demonstrating the power of these three strategies.

Here are 3 RRSP strategies for this season:

The Flat Shoe:

Put money into your RRSP. Period.

Most Canadians don’t.

23.4% of taxfilers in 2013 according to Stats Canada contributed to an RRSP!

And fair enough, if you aren’t making much in the way of income, I wouldn’t recommend it and would use an alternative shoe for saving – however, most Canadians don’t even save on a regular basis in any account – RRSP or not!

So here’s the point: Save. Save monthly if you can – dollar cost averaging is always best!

If you are in the top marginal tax bracket, it is one of the few tax deductions available to you if you are an employee – so just do it. Put on the FLAT shoe and do it. Otherwise, you are basically barefoot!

IMPORTANT – Don’t miss this paragraph! Here are the numbers: I’m going to use an example of a client saving $10,000 a year for all my examples. If you put in $10,000 to your RRSP and you are in the top marginal tax bracket (approx. 40%) you will get a refund of approx. $4,000 in Alberta – varies province to province and by how much income you actually make. Any accountant can help you calculate this amount for your personal tax situation or your financial planner can do that as well. The money in your RRSP grows tax deferred until you pull it out, and then it is taxed fully as your income at that time.

The Kitten Heel:

Wanna spice up your savings and go out on the town in a comfortable kitten heel? This is an easy boost in your RRSP savings, still only saving $10,000 a year.

Figure out how much you are getting back as a tax return. In the example above, you were getting back $4,000.

Because you know you are getting that $4,000 as a tax refund, why not invest it when you get it. If you do re-invest your return money and continue to do that over the years, you will now invest $14,000 every year, instead of the $10,000 you are saving up.

It will boost your savings by about 40% – that’s HUGE over the years. See the chart at bottom of post.

Or if you really need new shoes for that new trip – why not re-invest at least half of it, and blow the rest like you normally do. You will still get a 20% boost on your savings. I know my girls need a little quality shopping time too!

The Stiletto:

Ready to rock and make your portfolio extra hot? This is the ultimate RRSP strategy to boost your savings and make your portfolio sizzle!

Same $10,000 saved. Same example, but this time, we know already that we are going to put in $10,000 and get refunded $4,000.

So what do you do?

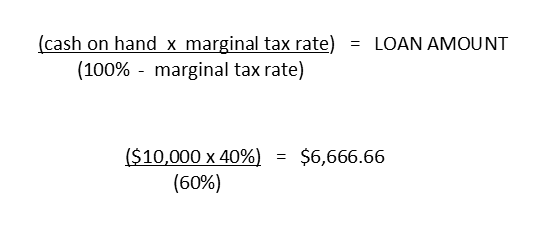

You get an RRSP Loan for $6,666.66 during that current tax year. (Yes – I know – I picked bad example numbers! YIKES!)

You invested $10,000 plus the $6,666.66 loan for a total of $16,666.66 into your RRSP.

Your tax refund is $6,666.66, which we use to pay off the RRSP loan we took out.

Here’s the fancy schmancy math formula that provided us with the loan amount needed to equal the tax refund:

Here’s an example: let’s say it’s December 2015. You have your $10,000 RRSP money saved in your bank account (or if you are smart, you’ve been investing a little every month dollar-cost-averaging!) Either way, you call me up – yes, your trusted financial advisor and I will hook you up with an RRSP loan from one of MANY financial institutions (RRSP loans are easy to get, very inexpensive and very short term – typically 2-3 months in duration, from the time you take it out, until you file your return and get your refund and pay it back.)

Then you take out an RRSP loan for $6,666.66

Then you file your taxes.

You receive a tax refund in the amount of $6,666.66 because you put into your RRSP $16,666.66! ($10,000 you had plus loan of $6,666.66)

That’s a boost of 66.66% into your retirement savings! (See chart below to see how your retirement saving look over time!)

The loan for a couple months may cost you $40-$100 (about $22 a month at 4%) interest only payments on a loan of $6,666.66. Small Potatoes!

I’m not sure why most people don’t do this. Oh yeah…. Now I know why – BECA– USE my industry does a BAD job of sharing this powerful strategy!!

Guess what! In all 3 scenarios – you still saved $10,000. No more, no less.

THIS STRATEGY IS HUGE GIRLS!!!

(Be a smarty pants and show this to your husband or show off at next office cocktail party!)

This also works with any amount you have saved for your RRSP. I can do RRSP loans as small as $1000 – so there are no excuses for you not to boost your RRSP savings by doing either “heeled” strategy – kitten or stiletto!

When you do any of these strategies or want help with your RRSP planning – call me! I don’t just value financial planning, I also value a good shopping spree and wine. Who said you can’t have it all.

You can have it all – with some smart planning!

PS. I’ve decided my boy clients need to see this also, so I may have to re-do this whole post with a car or sports analogy and send it to them. Ughhhhh………… 😉

WANNA SEE THE FINAL NUMBERS???

(I’m assuming you invest this money once annually with 6% annual compound growth at the end of the year for a client saving $10,000 every year utilizing the 3 strategies with a marginal tax bracket of 40%)

The Small Print: The information contained herein is based on certain assumptions and is for illustration purposes only.

While care is taken in the preparation of this chart, no warranty is made as to the accuracy or applicability in any particular case.

Please speak to your accountant and/or financial advisor regarding your own tax situation or before you implement any of these strategies.

You need to have sufficient contribution room available to utilize these strategies.

NEED RRSPs?

Have RRSPs and want to boost your RRSP savings by utilizing one of these strategies?

Make good money and this still sounds GREEK to you but you think you need to look further into this?

CONTACT ME & I’ll hook you up with a

KICK-ASSets RRSP PLAN!

403-875-0123 or lisa@ellementsgroup.com