THE CYCLE OF INVESTOR EMOTIONS

As a women, I know nothing about being emotional.

Nothing.

I’m the most steady constant person you will meet.

SAID NO WOMAN EVER!

Yup, I’m a total emotional rollercoaster somedays (okay, okay, everyhour of everyday! 🙂 ) Infact, one day they will probably add the word “syndrome” after my name.

And right now is no exception, on top of normal everyday stresses and emotions, come the emotions of what is going on in the markets and the economy.

When the economy is “bad”, clients also begin to freak out more about their portfolios as well, and as a financial coach, my job is to make sure you don’t succumb to fear, desperation, panic, despondency, and depression or at least don’t act upon them without taking the emotions out.

Instead, I’m going to share with you my hope, optimism and excitement and give you a thrill while at it (or that’s my goal anyways!)

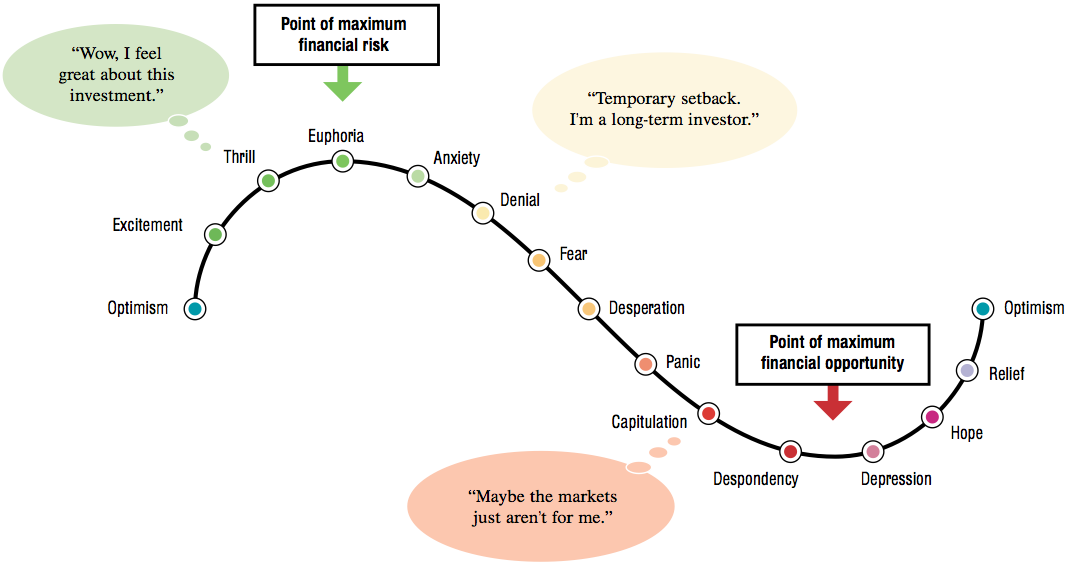

This chart outlines the cycle of emotions we feel when investing and important to note that emotions usually get in the way of a good financial plan.

THE CYCLE OF MARKET EMOTIONS CHART

This is the emotional psychology behind investing or the feelings an investor feels as they go through the investment cycle.

The point of maximum financial opportunity is ideally where you should buy, although typically when we should be buying our emotions and feelings are running the ship and steer us the wrong way because we are feeling fear, desperation and panic and in no way will emotion let logic take over and run the ship. Emotion at this point is like Lisa and her Cadbury Fruit & Nut Chocolate Bar – you dare not get in between us if you want to live!

The point of maximum financial risk is when everything seems to be going fantastic and everyone agrees with you. That is when you should sell, although at that point the champagne is flowing and the party is in full swing, so why sell your position and bring that great “feeling” to a complete stop.

As humans, the FOMO (Fear of Missing Out) drives us to do crazy things sometimes in relation to investing and this typically happens when we are close to the top of a market or sitting at or around “THRILL”. Especially when everyone is having a party and telling you to jump on the bandwagon and buy that bio-tech company that will be like winning the lottery. I relate FOMO to sneaking out with my roommate in college past curfew to meet up at a pub with some cute guys from our dorm. Sleep is over rated anyways.

FOMO has always been my thing – it actually pushes us forward and to try new things. So it’s not always a bad thing, it’s just something to be aware of, and when it comes to investing, maybe try to take emotion and fear out the equation and let logic prevail. I know this is MUCH easier said than done, especially when in college and even more so when everyone around you will be a millionaire before you if you don’t invest in that hot stock or real estate right now.

Then we swing to the other side of market emotions where FOF (Fear of Failure) is presumed. This is where we have “failed” in our heads and feel the need to sell and get out, cut our losses and move forward. This isn’t always the best approach – don’t get me wrong there are many times in life we need to cut our losses and move forward. This is when I caution you to let logic prevail and add in your 6th sense (women have powerful 6th senses!) – trust your gut.

Also, having a financial plan or Investment Policy Statement (IPS) will also help make sure you have a plan in place. As advisors, we create these for you so when you are “freaking out” we can remind you of the plan we put in place to help weather the storm.

Don’t forget: Storms are needed in life. Storms are what makes us appreciate the good times. If you never feel the bottom then you will never know the highs. So these cycles are good things. Be thankful for your trials, because let me be the first to tell you a whole lotta rainbows are coming your way soon!

BOTTOM LINE: So when fear of missing out, fear of failure, fear that the economy will collapse, or fear of any kind, rares its ugly head then it’s time to re-frame our brains, add logic and strip away crazy emotion this will probably help lead to better financial decisions and hopefully get rid of the impending doom and take appropriate action.